How NSW species credit trading has changed

The state-wide market for BOS species credits has grown and changed shape since the first transfers were recorded in 2020. This blog provides the background you need to understand current market trends.

Trading volume grew quickly, then steadied

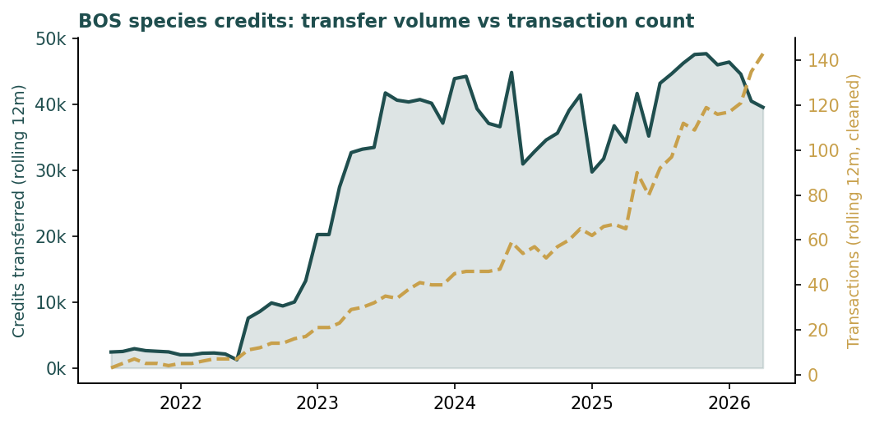

Recorded species credit transfers were negligible in 2020 and 2021, with fewer than ten trades a year. Activity stepped up sharply from 2022 and has climbed every year since on a rolling basis. Measured over a rolling twelve-month window, transferred volume rose from under 3,000 credits in early 2022 to a peak near 47,600 credits in late 2025, before easing back to around 39,500 by 31 March 2026.

The number of transactions tells a slightly different story from the volume. The rolling twelve-month transaction count has continued rising even as volume flattened and then eased, reaching 143 by March 2026. In other words, the market has kept getting busier in deal terms even as the total quantity of credits changing hands levelled off.

Figure 1. Rolling twelve-month transferred volume (credits) against cleaned transaction count. Volume peaked in late 2025; transaction count kept climbing.

The market broadened across many more species

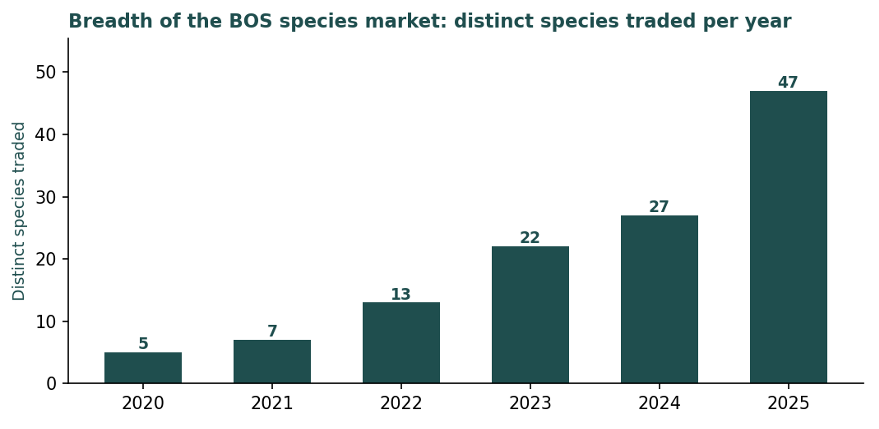

The most striking change is in breadth. In 2022, species credit transfers covered 13 distinct species across the year. By 2025 that had risen to 47 distinct species — more than a threefold increase in the number of species actually changing hands. The market has gone from a handful of well-known names to a much wider cross-section of listed species.

Figure 2. Distinct species transferred per calendar year. 2026 omitted as a part-year.

Parcels are getting smaller

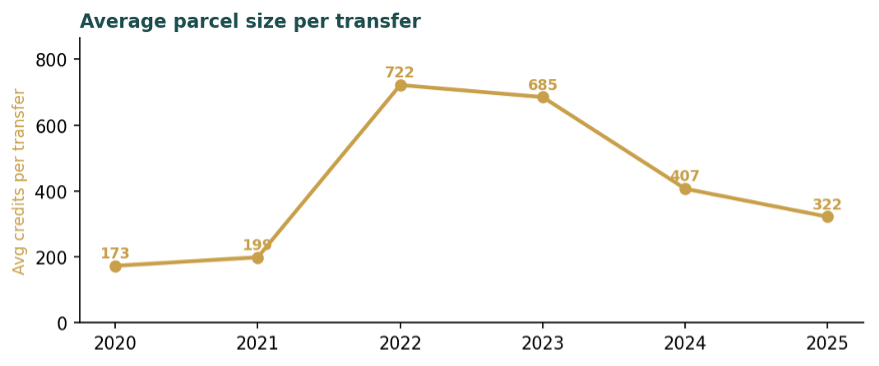

As more species and more transactions entered the market, the average size of each transfer fell. The mean parcel dropped from roughly 720 credits per transfer in 2022 to around 320 in 2025, and the median parcel has sat near 100 credits since 2024. The market in 2025 was made up of many more, individually smaller trades than the market in 2022 — consistent with the rising transaction count against flatter volume.

Figure 3. Average credits per transfer by year. 2026 omitted as a part-year.

Transfers by year

The transfer record shows a market growing in both scale and breadth. Annual transfers rose from single figures in 2020 to well over a hundred by 2025, and the number of distinct species changing hands widened from a handful to several dozen over the same period. Average credits per transfer peaked in 2022–2023, when a small number of large transactions dominated, then fell as activity broadened across more, smaller transfers. The Speargrass weighted price moved steadily upward across the period.

| Year | Transfers | Credits | Distinct species | Avg credits/transfer | Speargrass price |

|---|---|---|---|---|---|

| 2020 | 8 | 1,384 | 5 | 173 | $330 |

| 2021 | 10 | 1,990 | 7 | 199 | $336 |

| 2022 | 28 | 20,211 | 13 | 722 | $675 |

| 2023 | 64 | 43,849 | 22 | 685 | $499 |

| 2024 | 73 | 29,700 | 27 | 407 | $833 |

| 2025 | 144 | 46,357 | 47 | 322 | $877 |

| 2026 * | 46 | 3,600 | 24 | 78 | $902 |

* 2026 covers 1 January to 31 March only and is not comparable to the full years above.

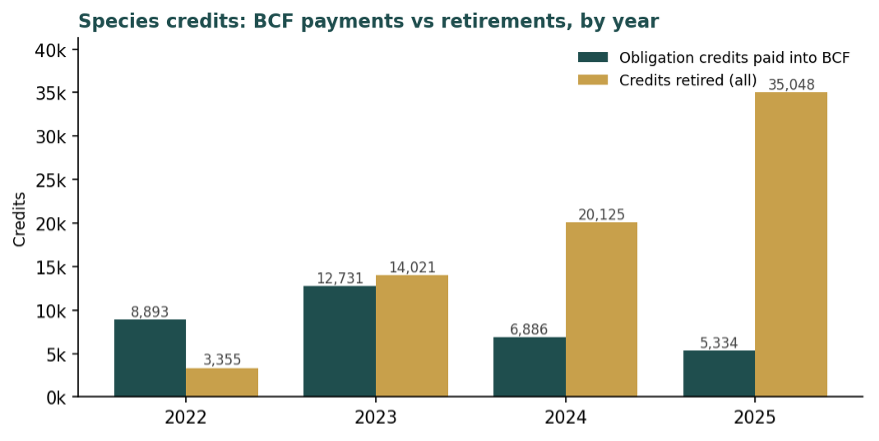

Two ways obligations are met: the fund and the market

A developer with a species credit obligation can meet it in more than one way: by buying and retiring credits directly, or by paying into the Biodiversity Conservation Fund (BCF) and transferring the obligation to the Biodiversity Conservation Trust, which then secures and retires credits — or equivalent offsets — on the developer's behalf. The transfer and retirement figures above capture market activity; the fund is a separate channel that sits alongside it.

The two series below are shown side by side, not netted against each other. They are deliberately not reconciled, for reasons set out beneath the chart.

Figure 4. Species credit obligations paid into the BCF (by quote year) against all species credits retired (by year).

On the payment side, obligations covering roughly 33,800 species credits were paid into the fund across the window for which quote data exists (October 2022 to December 2025), with a combined obligation value near $79 million. Paid-in obligation volume peaked in 2023 and has fallen each year since. On the retirement side, recorded species retirements rose over the same period, from around 3,400 credits in 2022 to roughly 35,000 in 2025.

Retirements and the Conservation Trust

Within the retirement record, the stated basis for each retirement is itself informative. In the earlier years a large share of retirement events referenced the Biodiversity Conservation Trust acquitting an obligation, rather than a developer retiring directly — consistent with the fund channel described above. The proportion of retirements attributed to the Trust was high in 2020–2022 and declined in proportional terms as the overall number of direct commercial retirements grew.

| Year | Retirement events | Credits retired | Distinct species | BCT-attributed events |

|---|---|---|---|---|

| 2020 | 3 | 543 | 3 | 2 |

| 2021 | 7 | 745 | 6 | 5 |

| 2022 | 33 | 3,355 | 7 | 28 |

| 2023 | 43 | 14,021 | 18 | 17 |

| 2024 | 100 | 20,125 | 22 | 53 |

| 2025 | 87 | 35,048 | 34 | 7 |

| 2026 * | 18 | 2,349 | 12 | 11 |

* 2026 covers 1 January to 31 March only and is not comparable to the full years above.

What the record shows

Across five years, the BOS species credit market has grown from a near-dormant handful of trades into a busier, broader and more granular market: more transactions, many more species, and smaller individual parcels, with rolling volume now off its late-2025 peak.

Retirements have grown in parallel, obligations continue to be routed through both the market and the conservation fund, and the mix of retirement bases recorded in the register has shifted over time.

The data and analysis presented are drawn from multiple sources, including: NSW Government public registers (such as the BOS Credit Transaction Register and Biodiversity Conservation Fund Charge Quote Reports), Biodiversity Conservation Trust (BCT) reports, and Other publicly available or Speargrass-compiled datasets. Payment and retirement series are not reconciled. Calendar-year 2026 is a part-year. For pricing, valuation or bespoke information on a specific credit, contact Speargrass.